Private practices make $4000 or more profit off of each pair of premium aids. Why do they mark them up so high? Because we accept that price and have no other place to go to purchase an assortment of quality aids. There are 1000s of hearing aid dispensers (Audiologists and Hearing Instrument Specialists). Many sell less than 20 aids per month. To make a living, they need a high profit per aid. This post analyzes a hypothetical company NEWCO to find out what characteristics such a company needs so that it is profitiable while being equitable to its customers.

Question

Can a company that sells the same premium aids used in the VA, has a volume similar to the VA (560,000 aids/year) and has the same or better service as the VA and private practices, sell those aids and services at 25% to 50% the prices demanded by private practices?

Description

This post describes a hypothetical company (call it NEWCO) and compares Profit/Loss sheets of it and Status Quo practices. NEWCO has a central facility that negotiates contracts with manufacturers, handles national advertising for the franchises, supplies accounting and customer relations software (web-based) to the franchises, trains franchise staff, and makes sure uniform pricing and services are provided to customers. The analysis assumes the negotiated, factory price for a premium hearing aid averages $350 each – a little over the average price recently offered to the VA by a number of the best manufacturers (1, 2).

The franchises are full service. They have a VA-range of hearing aids to best fit physical and acoustical needs of their customers. The staff provides hearing exams, fitting, and adjustments as needed. They also run a support group that meets alternate weeks. Attendees learn from invited experts in the field of hearing loss, share experiences and insights with each other, and talk to attending franchise staff members.

The franchises are unbundled. They charge $100 for the hearing exam (1 hour), $100 for the selection and fitting (2 hours, possibly two visits), and $50 for each 30-minute adjustment and extra visits (30-minutes) as needed. If one wants to join the biweekly two-hour support group (and one can do it anytime) -- it costs $50/year. The cost for one exam, one fitting, three adjustments and two selected hearing aids is charged up front. If the customer returns the hearing aids within the trial period, she gets a full refund less the cost of services rendered.

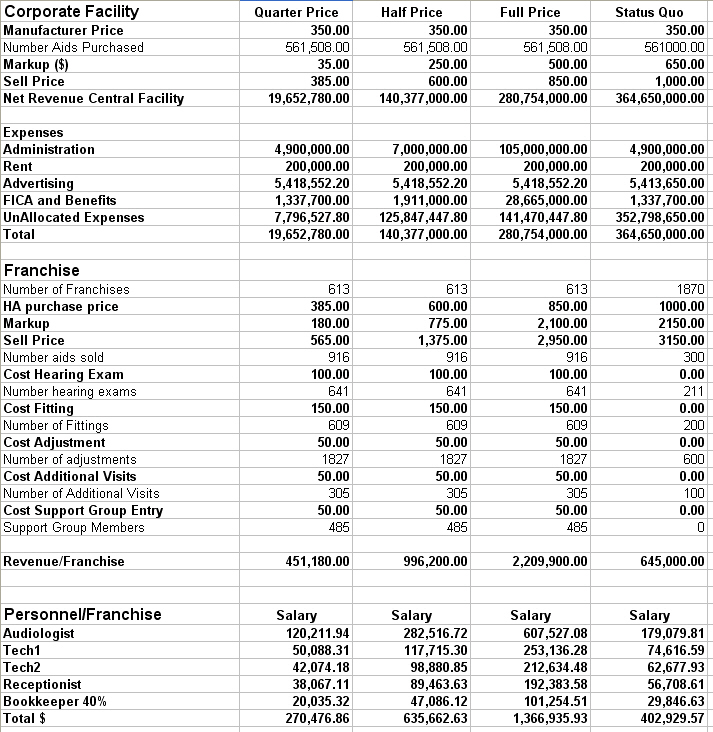

Comparison of Profit/Loss Statements Shown Below

The revenue and expenses of the status quo and NEWCO are compared when NEWCO charges 25%, 50%, and 100% of status quo prices. For example, in the Quarter-Price Column of the analysis below, the customer pays $1,530 for two premium aids, exam, fitting, and three adjustments, approximately 25% the price offered to the author by private practice audiologists.

The fourth column “Status Quo” assumes bundled, current prices. Income is totally from aid markup. In all cases, the analysis assumes the corporation or buying group purchases approximately 560,000 aids per year – the same number recently purchased by the Veterans Administration (2). The 560,000 aids represent 25% of the current number of aids purchased in the non-VA U.S.

Workload

a) NEWCO

For a franchise to sell 916 aids a year, I assumed the following activities:

1) Each customer purchased two aids meaning 458 customers purchased aids.

To do this:

a) 641 hearing exams were given

b) 609 fittings were performed along with 1827 adjustments

c) 305 additional visits were performed

d) 25 two-hour support groups were led by two staff members.

The total number of staff hours to do the above were 3025 out of 5040 possible which meant each audiologist or technician spent 4.2 hours per working day with a patient. A year is considered to be 48 weeks of 7 hours/day, 5 days/week.

b) Typical Audiologist Private Practice

The analysis assumes the buying group sells a premium aid for $1000. Discounts and kickbacks are not considered. The private practice sells aids for $3150 each. They sell 300 aids/year per outlet, but with the high markup they still get sizable salaries of $179k for the lead audiologist and $74k and $62.6k for the two hearing-aid technicians. A more typical staffing is two audiologists with the second one earning the sum ($137.3k) of the two tech salaries. This means more contact hours for the two audiologists but since the outlet is selling only 300 aids, the contact hours are 1.3 hours/day each for 3 staff members or 2 hours/day each for a staff of 2. This assumes they sell to 150 patients in one year, give 211 hearing exams, 200 fittings, 600 adjustments and 100 extra visits. They do not offer a support group and thus do not spend the extra 100 staff hours as do the NEWCO franchises.

Major revenue and expenses are categorized. Other expenses, including bonuses and distributions to stakeholders, are placed in Unallocated Expenses.

The Profit/Loss Statement Description in more detail

The Quarter Price Column

In the 25% Price column the corporate facility buys aids for $350 each and sells them to the franchise for $385 each. After paying $4.9M in salaries to corporate employees, $200,000 rent, $5.4M in national advertising, $1.3M in payroll taxes and employee benefits, it still has $7.8M in unallocated expenses most of which is reinvested for growth/maintenance and distributed to owners.

The 613 franchises buy the aids for $385 each and sell them for $565 each. They also charge for their services of exams, fittings, adjustments and other hearing issues that benefit their customers. The revenue of each franchise (assuming it sells 916 aids to 458 customers over one year along with services) is $451,180. The lead audiologist makes $120,000 per year plus $14,425 in retirement and medical benefits. The salaries of the staff total $270,476. After the common expenses of rent, equipment purchase/repair, advertising, salaries, payroll taxes, and benefits, the franchise has $11,111 for reinvestment and profits. This may be on the lean side. Let’s look at the statement for a NEWCO where the customer gets services and aids for half the price charged in private practice.

The Half Price Column

In this case corporate sells the aids for $600 each and even after paying significantly higher salaries, corporate now has $140M available for unallocated expenses including reinvestment and distributions to owners (stakeholders).

The Franchise pays $600 for the aid and sells it for $1,375 as well as charges for its services. In this case the lead audiologist gets $282,515 in salary and $32,902 in retirement and health benefits. The rest of the staff gets more as well. The expenses allowed higher rent, equipment costs, and advertising charges and still has unallocated expenses of $26,912. The salaries are on the cushy side.

The Full Price Column

The profits and salaries are outrageously high.

The Status Quo Column

The buyer’s group purchases hearing aids for $350 each and sells them to the private practice for $1000 each. The revenue for the buyer’s group is $364M and has unallocated expenses of $352M for reinvestment and distribution to stakeholders. One may argue that the buyer’s group cannot negotiate as well as the VA even though they are buying the same volume under the similar distribution rules. Even if the buyer’s group paid $700/aid their net revenue would be $168M. This would cover expenses with a lot leftover for the stakeholders.

The private practice pays $1000 for an aid and sells it for $3150. No additional charge for services. If a private practice of two audiologists and support staff sold to 458 customers a year (The NEWCO number of customers/franchise), the two Status Quo audiologists would have to each work 6.1 hours/day and each make $706,000 per year including benefits. They don’t attract that many customers. In this analysis we assume 1870 practices each selling 300 aids/year (150 customers) and the salary of the lead audiologist to be $179,000. It is interesting to note that in this case a practice with two audiologists selling 300 aids per year only requires 2 hours/day for each audiologist.

Conclusion

The NEWCO salaries and profits are ample when selling premium aids and full service to consumers with retail costs between 25% and 50% of the Status Quo offerings. The existing dispensing system burdens those who wear hearing aids and adds further deterrence to 75-80% of those needing aids from purchasing them. The excessive cost is magnified by the fact that aids last only 4-5 years.

No comments:

Post a Comment